Step 1 - Finding the Appropriate ETFs (and Possibly Mutual Funds)

The search for investments to buy for a portfolio begins with a hole to fill. Usually, that is based on an intended asset allocation (see our long ago posts on Asset Allocation and others in June and July 2008 on the planning process that precedes a purchase decision). In this test, we chose as an example to look for Canadian Equity ETFs in order to do some nitty gritty assessment.

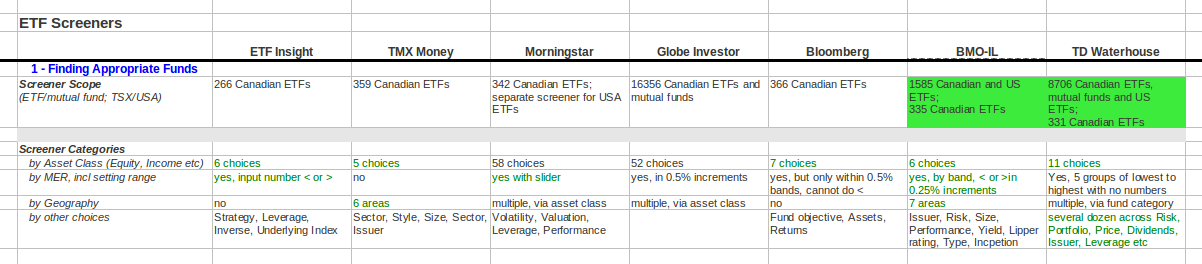

The Screeners

Our seven screeners are:

The table below shows how they stack up in the process of narrowing down the search. Green text shows where a screener provides capabilities that we think are helpful, while green highlighted cells show where something we think is really important is done really well.

Step 2 - Analyzing the Options

The same overall result comes out of the next step of comparing the alternatives - BMO and TD are appreciably ahead of the pack. See all the green under their columns in the table below.

We found their side-by-side comparison feature, which none of the other screeners have, to be a powerful time-saver. The ability to scan down a list of key characteristics such as Management Expense Ratio (MER), returns, volatility, composition of holdings and tracking error, instead of laboriously opening detail sheets for each ETF in turn, is a massive convenience. In addition, on most of the other factors, BMO and TD does as well as, or better than, their rivals. An exception, curiously, is that they both are missing the crucial MER for one of the mainstream Canadian equity ETFs, the PowerShares FTSE RAFI Canadian Fundamental Index (TSX symbol: PXC). ETF Insight, Morningstar and Globe Investor all have the MER. TMX Money is worse though - it shows the MER for the wrong fund.

There are other errors in the data we found - some MERs and returns. The moral of the story is that nothing is perfect, there are errors in data. For important numbers, it is a good idea to check several sources.

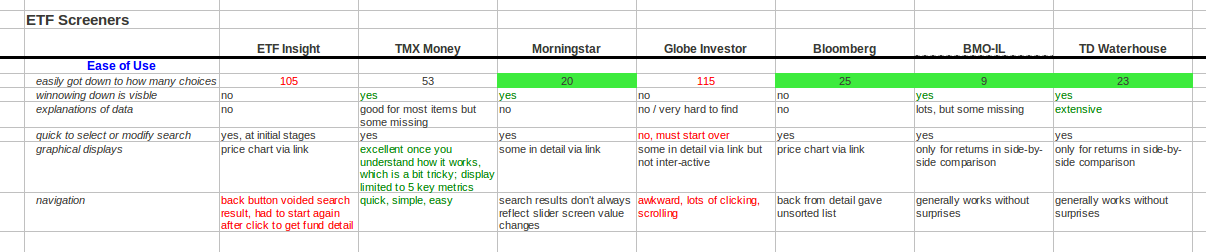

Ease of Use

Some of the screeners ended up being pleasant to use, while others became frustrating. Our table below shows what we found.

The ability to quickly get down to a manageable number of ETFs when doing our Canadian equity search became more significant as we passed from one screener to another knowing exactly what we wanted and what should come out. Again, the green highlight cells show the best screeners. They quickly spit out about twenty ETFs, which fit on one screen and avoids clicking through multiple pages. Ending up with over 100 ETFs in a list is no help and it is annoying to spend a half hour exploring the ways to get the number down. On ease of use overall, Morningstar, Bloomberg, BMO and TD do a good job. If only TMX could more easily narrow the list of ETFs, its superior graphical and condensed, simple displays of results would make it outstanding.

Bottom Line

The free screeners provided as part of the standard discount broker account package capabilities from BMO Investorline and TD Waterhouse are fine tools and generally stronger than competing websites. Nevertheless they are not perfect in every way (is anything?) and the investor may benefit from cross-checking data with the other sites, or for obtaining unique data such as TMX's. For US ETFs, when preliminary screening involves US ETFs, some of the US-only websites may provide additional unique data.

Disclaimer: this post is my opinion only and should not be construed as investment advice. Readers should be aware that the above comparisons are not an investment recommendation. They rest on other sources, whose accuracy is not guaranteed and the article may not interpret such results correctly. Do your homework before making any decisions and consider consulting a professional advisor.